The Coordinating Council for Economic Development

The Coordinating Council for Economic Development, established in 1986 by the General Assembly, was formed in response to a general need for improved coordination of economic development efforts by those state agencies involved in the recruitment of new business and the expansion of current enterprises throughout the state. The Council consists of the heads or board chairs of 11 state agencies concerned with economic development: SC Department of Commerce, SC Ports Authority, SC Department of Parks, Recreation & Tourism, SC Department of Agriculture, SC Technical College System, SC Research Authority, SC Department of Employment and Workforce, SC Department of Revenue, Jobs for Economic Development Authority, SC Department of Transportation and Santee Cooper.

Grants

South Carolina has three discretionary grant funds that are administered by the South Carolina Coordinating Council for Economic Development. The Coordinating Council will evaluate each project on a case-by-case basis and a grant may be awarded by the Coordinating Council, in their sole discretion, depending on the needs of the project.

-

The Economic Development Set-Aside Program

The Economic Development Set-Aside Program

The Economic Development Set-Aside Program assists companies in locating or expanding in South Carolina through road or site improvements and other costs related to business location or expansion. Overseen by the Coordinating Council for Economic Development, it is the Council’s primary business development tool for assisting local governments with road, water/sewer infrastructure or site improvements related to business location or expansion.

-

Governor's Closing Fund

The Governor’s Closing Fund

The Governor’s Closing Fund was created in 2006 to assist when additional funding is necessary to recruit or retain in the state high impact economic development projects. The grants are generally awarded to assist with the costs of real property improvements or other road or infrastructure improvements. This fund is dependent on annual appropriations from the South Carolina General Assembly.

-

Rural Infrastructure Fund

Rural Infrastructure Fund

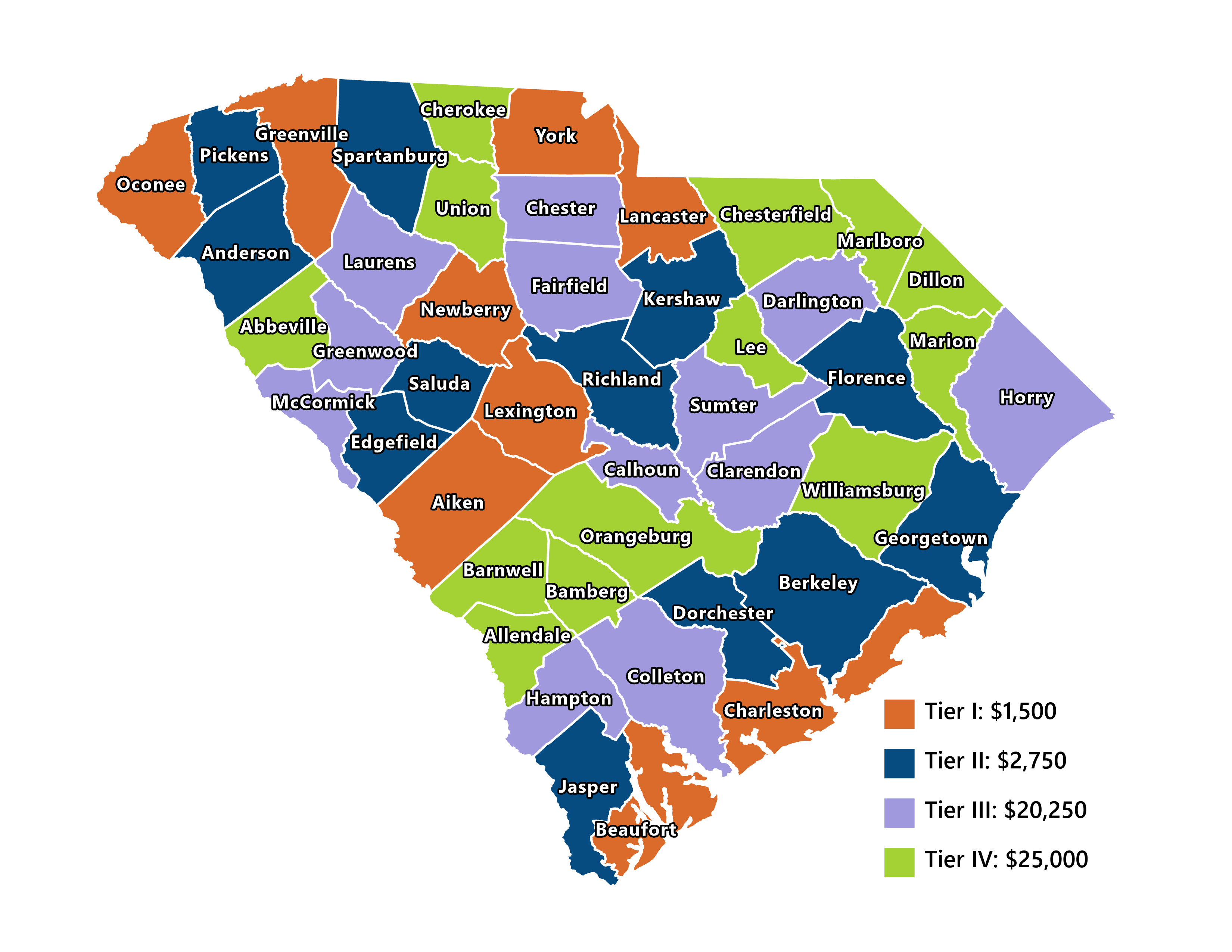

The Rural Infrastructure Fund (RIF) assists qualified counties in the state's rural areas by providing financial assistance for infrastructure and other activities that enhance economic growth and development. It can be used for job creation and/or product development. Qualified counties are designated as “Tier III” or “Tier IV” by the Department of Revenue and have received approval for an economic development strategic plan by the Coordinating Council for Economic Development. Click here to view the county tier map.

{kind=link}

Other Incentives

-

Job Development Credit

Job Development Credit

South Carolina’s Enterprise Program is substantially different from the state’s other tax incentives because it does not reduce a particular tax liability; instead, it provides companies with funds to offset the cost of locating or expanding a business facility in this state. Representing actual cash contributions to the project, this incentive allows South Carolina to lower the effective cost of investment and positively contribute to a company’s bottom line and profitability.

The Job Development Credit effectively uses the personal withholding taxes of new employees to reimburse qualified, approved companies that add value to South Carolina and the community in which they locate. These reimbursements are for eligible capital expenditures (land, building, site development, pollution control equipment or infrastructure) associated with projects creating new full-time jobs that also provide health care benefits for South Carolina citizens.

The South Carolina Coordinating Council for Economic Development administers the Enterprise Program. Funds for the Job Development Credits come from state personal income tax withholding that is paid by a company’s employees. Employees receive a credit equal to the withholding used by the company; therefore, there is no financial impact on employees. No company will be allowed to claim a credit on any employee whose job was created in this state before the taxable year in which a company was approved for the program. In addition, the Coordinating Council generally caps annual collection at no more than $3,250 per employee per year.

To verify capital expenditures and qualifying jobs, a company is required to make its payroll books and records available for inspection by the Coordinating Council and the Department of Revenue. In addition, a company must furnish a report prepared by the company that itemizes the sources and uses of the funds, and such report must be filed by June 30 following the calendar year in which the refunds are received.

Eligibility Requirements

To be eligible to apply for the Job Development Credit, a company must:

- Meet the requirements of a manufacturing and processing, corporate office, warehouse and distribution, research and development, agribusiness, tourism, or qualified service-related facility as required for the Jobs Tax Credit;

- Create at least 10 new, full-time jobs (or meet additional requirements if qualifying as a service facility);

- Provide full-time employees with a benefits package that includes a comprehensive health plan and pay at least 50% of an eligible employee’s cost of health plan premiums; and

- Pay a non-refundable $4,000 application fee, receive a positive cost/benefit certification (the project is of greater benefit than cost to the state) from the Coordinating Council, and pay a $500 annual renewal fee.

Please note that the Coordinating Council will generally only allow companies to collect credits for 10 years, and only on new full-time jobs with wages at or above the current county average wage for the county in which the project is located. Click here to view the county tier map.

The Revitalization Agreement. Once a company’s application for eligibility to receive Job Development Credits is approved by the Coordinating Council, the company will be required to enter into an agreement with the Coordinating Council called a Revitalization Agreement. The Revitalization Agreement is a contract with the state guaranteeing the company’s participation in the program, assuming it stays current with state taxes and meets its commitments on job creation and investment. Under the terms of the Revitalization Agreement, the Coordinating Council and the company:

- Establish mutually agreeable investment and employment minimums that the company must meet and maintain in order to claim a Job Development Credit;

- Sets a date by which the project’s investment and employment will be completed (must be within five years of the date of the agreement); and

- Identifies a maximum reimbursement amount.

-

Port Volume Increase Credit

Port Volume Increase Credit

South Carolina provides a possible credit against income taxes or withholding taxes to entities that use state port facilities and increase base port cargo volume by 5% over base-year totals. To qualify, a company must have 75 net tons of non-containerized cargo or 10 loaded TEUs transported through a South Carolina port for their base year.

The Coordinating Council has the sole discretion in determining eligibility for the credit and the amount and type of credit that a company may receive. The total amount of tax credits allowed to all qualifying companies is limited to $15 million per calendar year. A company must submit an application to the Coordinating Council to determine its qualification for, and the amount and type of, any tax credit it will receive.

-

Tax Credit for Increases in Purchases of South Carolina Agricultural Products

Tax Credit for Increases in Purchases of South Carolina Agricultural Products

South Carolina provides a possible income tax credit or withholding tax credit to agribusiness or agricultural packaging operations. To be eligible for this credit, a company must have a base year in which the company purchases more than $100,000 of agricultural products that have been certified as grown in South Carolina by the South Carolina Department of Agriculture (“SCDA”) and then must increase number of agricultural units purchased in the following year by at least 15% over base-year unit totals. The base-year unit amount will be re-calculated every year after the initial base year.

A company must submit an application to the Coordinating Council by no later than September 30 of the year following the year in which it increases purchases. Such application will be reviewed by the staff of the Coordinating Council and SCDA to determine eligibility. Based on the recommendation of SCDA the Coordinating Council will determine the amount of, and the type of any tax credit, the company will receive. The credit may not exceed $100,000 per taxpayer in any one year. The total amount of tax credits allowed to all qualifying companies is limited to $1,000,000 in 2019, $1,500,000 in 2020 and $2,000,000 in years thereafter. Any unused credits may be carried forward for 5 years.

-

Funds for Retraining Available Employee for Existing Industry

Funds for Retraining Available Employee for Existing Industry

Eligible businesses engaged in manufacturing, processing or technology intensive industry may be eligible for a refund of up to $1,000 per eligible full-time employees per year for retraining costs. The retraining must be necessary for the business to remain competitive or to introduce new technologies. An eligible employee is a production or technology first line employee or immediate supervisor who has been continuously employed by the company for at least two years. “Technology employee” includes an employee who is directly engaged in the design, development and introduction of new products or innovative manufacturing processes, or both, through the systematic application of scientific and technical knowledge at a technology intensive facility.

Please note that companies will not be allowed to claim Job Development Credits and Retraining Credits on the same employee.

The retraining must be approved and coordinated by the technical college(s) under the jurisdiction of the State Board for Technical and Comprehensive Education serving the designated region where the company is located. The technical college may provide the retraining program delivery directly or contract with other training entities to accomplish the required training outcomes.

Refunds per eligible employee for retraining may not exceed $1,000 in a year, or $5,000 over five years. The company must match $1.50 for each $1.00 of the employee’s withholding share used for training. The total amount is paid to the technical college providing the training. In order to collect funds for retraining, a company must pay an annual $250 renewal fee.

{kind=link}